Sepso points to several other games that incorporate metaverse elements, such as Roblox, Fortnite, Second Life and Microsoft’s Minecraft. On those platforms, players can teleport between millions of games, build virtual social spaces and even attend concerts — all while purchasing virtual stuff to heighten the experience. Most of these types of games require VR headsets and consoles, which favors Microsoft, with its HoloLens and Xbox hardware.That’s where Microsoft’s software, cloud computing, gaming and virtual technologies position the company well. And adding Activision’s gaming capabilities only enhances its outlook.

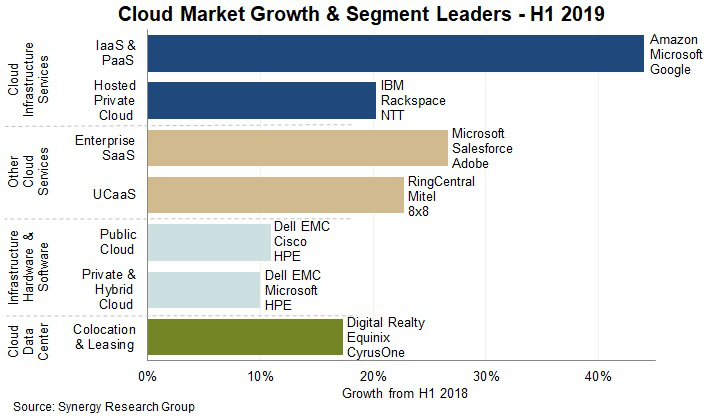

According to Gartner, the market is dominated by five vendors who account for nearly 80% of worldwide IaaS cloud market share in 2018. These vendors are Amazon (47.8%), Microsoft (15.5%), Alibaba (7.7%), Google (4.0%) and IBM (1.8%).